How to check my credit score in South Africa

Before you can fix a bad credit score you must first figure out what it is.

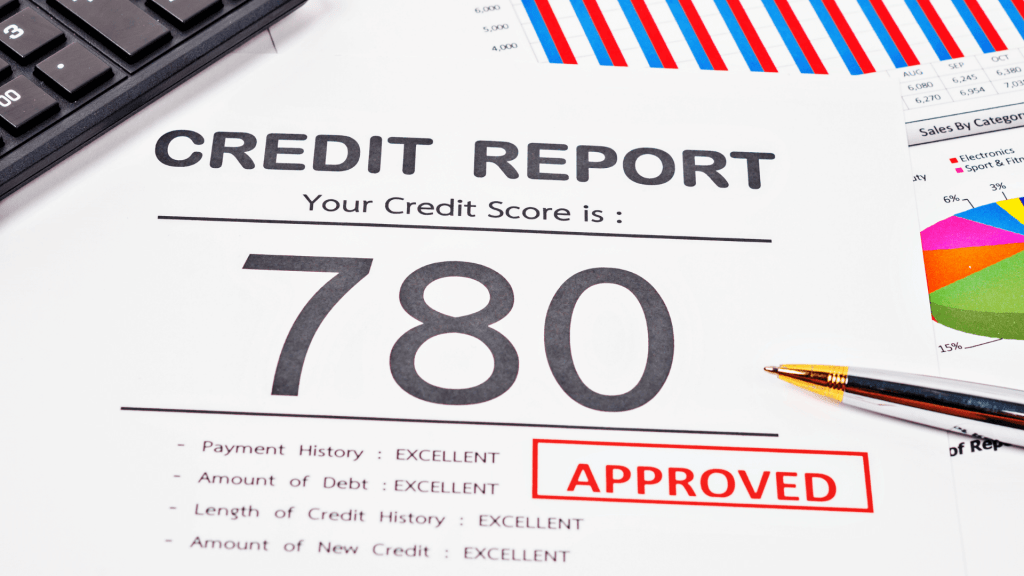

The first step in fixing a bad credit score is to find out exactly where you are. You can do this by getting a free copy of your credit report from the South African Credit Bureau (SACB).

A credit report contains all the details about your borrowing history and current financial situation, including:

- The amount of debt you currently have, if any

- Your payment history with creditors such as banks and lenders

- How much money you owe, including how much is owed on each account and how often you pay off your debts

Your credit score is a number between 0 and 2000, with the lower the score, the worse your current level of creditworthiness.

Your credit score is updated by credit bureaus every month. It can be accessed by various service providers such as banks, insurance companies and telcos.

You can access your free annual report from www.creditsuisse.co.za or www.mycreditfilexplorer.co.za

Your financial conduct is rated by two institutions in South Africa TransUnion ITC and Experian.

Your financial conduct is rated by two institutions in South Africa TransUnion ITC and Experian.

The two credit bureaus in South Africa are TransUnion ITC and Experian.

They are both free to access and you can access them from your phone, tablet or laptop.

They will provide you with your credit score and a report on your credit history.

A good credit score is one that will allow you to qualify for more competitive interest rates from lenders.

A good credit score is one that will allow you to qualify for more competitive interest rates from lenders. A score of 720 or higher is considered excellent, while a score between 700 and 719 is very good. If your score falls between 600 and 699, it’s still considered a decent rating but you may have trouble qualifying for loans with the best terms (particularly if you’re looking at car loans). In the lower ranges of 509 to 599 and 496 to 598, lenders may be reluctant to offer credit cards or other types of unsecured debt at all—or else they’ll likely charge high interest rates.

If your credit history shows that it’s been quite some time since any mistakes on your record were corrected. This can also move up or down your overall score. It all depends on whether it’s reflected positively or negatively in relation to other aspects of your financial life.

The most basic way to check your credit record and find out what your credit score is. By going directly to the TransUnion and Experian websites.

To check your credit score, you have to know the difference between checking and monitoring your credit report. A credit report is a record of all loans and debts that you have taken in the past and how well you have paid them back. It can include things like how much money you owe, or are any judgments against you. It could also be for non-payment of debts and whether or not there has been fraud on any accounts (i.e., identity theft).

A credit score is an algorithm based on this data which shows a person’s likelihood of defaulting on debt repayment or incurring more debt than they can pay off in time. This means that even if someone has paid off their debts without being late on payments, they may still end up with a bad credit score simply because they didn’t show enough restraint when it came to taking out new loans or making purchases using other people’s money (via loans).

There are several ways to check your credit score in South Africa, including on the TransUnion and Experian sites.

There are several ways to check your credit score in South Africa, including on the TransUnion and Experian sites.

You can also access it by going through a credit bureau and requesting it from them directly. Your credit report will have all the information about your credit history and you’ll be able to see what rating you have based on that information.

The difference between a credit report and a credit score is that the latter is an individual number that represents how well or poorly you’ve managed your finances over time (and how likely it is that they’ll continue to do so). A high score indicates that you’re more likely than someone with lower marks to repay any loans made based on their recommendations; conversely, low scores suggest less favorable repayment outcomes among those who borrow money using whatever criteria were used when calculating their scores (e.g., age range).

Finally, keep in mind that although “credit rating” refers specifically to one particular type of rating system. It was employed by companies such as Moody’s Investors Service or Standard & Poor’s Rating Services—and may sometimes even refer specifically to these particular companies themselves—it doesn’t mean anything like what people usually mean when they say something like “I’m not sure if I should trust this person because his rating was too high.”